Can AI Save Tech-Enabled Services Startups?

Why these startups have struggled and how AI can help

It has been a rough few years for “Tech-Enabled Services”1 startups. Arguing that better technology could revolutionize old school services businesses, these startups have tackled labor intensive industries like healthcare, renovation, hospitality, finance, law and more. But big successes have been rare. Few companies have gone public and those that have are often worth little more than their invested capital (ex: Lemonade, Compass, Oscar Health, Talkspace) or much less (Better Mortgage, Sonder).2 Last year, some VCs were labeling the category “dead/unfundable.”

But there’s hope on the horizon. AI will revolutionize software development and help automate labor intensive tasks. As a result, investors are as excited as ever about “AI-Enabled Services” startups.

I’m similarly bullish. AI can solve one of the key reasons that tech-enabled services startups have struggled and AI is uniquely positioned to help these startups, not incumbents. Before getting into why AI can help, it’s important to understand why tech-enabled services startups have struggled so much in the first place.

Why tech-enabled services startups have struggled

AI has the potential to solve one of the biggest problems tech-enabled services startups have faced: it costs a lot of money to build homegrown software in services industries and these businesses have low margins due to high operational costs. This combo means tech-enabled services startups often never get enough scale to fund their R&D costs and become profitable.3

Building software is too expensive for tech-enabled services startups

Building software is expensive for any startup. Engineers, designers and product managers cost a lot of money. But it’s been even more costly for tech-enabled services startups because of the broad scope of the products they are building and the challenge of building software in operationally complex and often heavily regulated industries.

Let’s say you are building a health insurer from scratch like Oscar did. You aren’t a pure SaaS company which has the liberty of building software for just one part of the health insurance workflow to start - to service customers, you need software which can handle all aspects of being a health insurer (customer, provider, claims, etc.) and meets all compliance requirements from day 1. You can’t build this overnight, so in practice you are forced to rely on external vendors/software providers initially (Oscar’s progression is detailed here). But these external providers are usually clunky, hard to integrate with and add tech debt to your product. These dynamics add additional cost and complexity and mean you need large product/engineering headcount to build out even in initial versions of your product.

Adding to the challenge, a lot of services businesses are complex operationally and often heavily regulated. Building software for operationally complex workflows, while not a challenging technical problem like building an LLM, is still challenging in a different way. You need your tech and operations teams to work smoothly together and for tech teams to deeply understand how different operational processes work. On top of this, you sometimes have a large regulatory burden. If you’re a health insurer, your software needs to internalize thousands of pages of federal and state guidelines. Your legal team needs to be big, but so do your engineering and product teams to ensure your products are satisfying all these regulations.4

R&D costs are lower for incumbents

Importantly, R&D costs are often lower (as a share of revenue) for incumbents. For health insurance incumbents (like United Healthcare), you benefit from having an already built system (however bad it is) and can focus more on maintenance and upkeep of your software which is cheaper. Because R&D costs are somewhat fixed, incumbents also benefit from their size and being able to spend more on R&D in absolute $ but less as a % of revenue.

In more fragmented markets, smaller incumbents don’t build their own software but can often buy off the shelf software for a small share of revenue. For example, there have been a few tech-enabled home renovation startups that have popped up (example). These startups have high R&D costs and are competing with small, local contractor businesses which may have 10 employees and are paying a fairly low % of their revenue to ServiceTitan to run their business. Or similarly, a company like Sonder has to compete with a local Airbnb host who has minimal overhead.

High operations costs eat into margins

If you have high margins, like most SaaS businesses, then it becomes easier to pay for these R&D costs. But tech-enabled services businesses tend to have low margins due to high operations costs. Unlike pure SaaS companies, which naturally have very high gross margins, a large share of revenue for services businesses often goes to paying people to just conduct tasks in customer support, back office operations, compliance and similar functions.

This has been part of the opportunity of these startups: if you can automate a lot of the human tasks, you could theoretically improve margins significantly. But many startups have struggled to execute on this vision, as tech startups are often bad at managing operations and even if you improve margins, it’s been difficult to get margins as high as traditional SaaS.

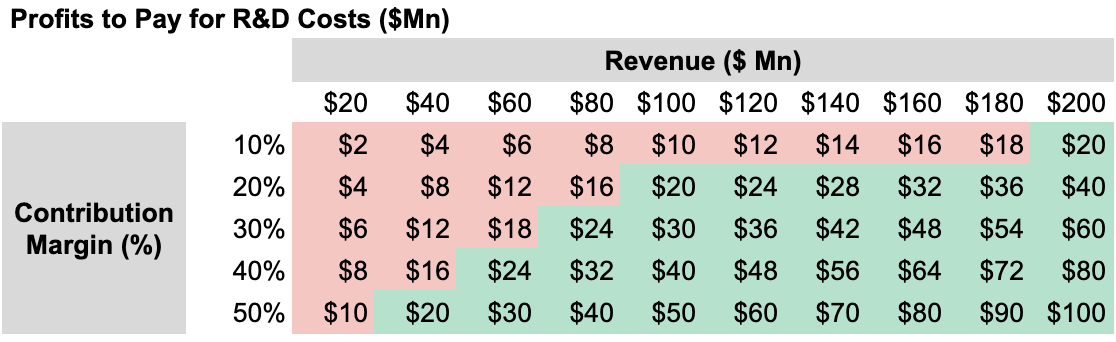

Most startups never hit the scale needed to fund R&D costs

Combining these two together (high R&D costs, low margins), you see the challenge tech-enabled services businesses have faced. To take our health insurance example again: let’s say your operations before R&D costs typically have a 10% margin and your “Tech” org costs $20m to run (100 people at 200k a year).5 Even if homegrown software improves these margins from 10% to 20%, you still need to get to >100m of revenue just to make any profit after paying for your R&D costs.

As a result, you often need to get really big to get your tech-enabled services startup to be remotely profitable. It’s possible - Oscar is one example recently which has gotten profitable and turned a corner. But it often takes a lot of capital and time and most startups just don’t last long enough.

AI can solve this problem

Can AI help solve this problem? I think so.

Improve R&D efficiency: AI can significantly improve the productivity of software engineers. AI copilots/agents will help, but I also think generative AI will be especially helpful to product managers building in services industries with complex operations and regulations.

One way of thinking about this is that traditionally, tech-enabled services startups would need to do too much costly “build” in the build/buy tradeoff when running their businesses. AI is going to change that math significantly and make building your own software and internal tools much cheaper.

Reduce operations costs: AI can also reduce the operations costs needed to run the business day to day. Customer support is one obvious example. Klarna claims to be able to handle 2/3rds of all customer support chats with AI.6 AI Agents in particular show promise to automate the types of operations workflows which require lots of humans to do today.

As a result, the amount of R&D investment needed to get to scale for these startups will go down and margins can improve significantly from automating operations workflows.7 We are going to enter a new age of opportunity for “AI-enabled” services startups.

A few caveats though:

AI will be much more impactful in services businesses which are white-collar work vs blue-collar work. AI will be effective at automating tasks humans do with computers (ex: insurance or law) but not as impactful for manual work done in the real world (ex: home renovations, hospitality, etc.).

AI also won’t solve all the problems these startups have faced, like distribution challenges. There are some interesting questions I’ll address in a follow-up piece about whether startups should buy larger incumbents (growth buyouts) or whether private equity type rollups make sense to solve for distribution.

A lot of the optimism around AI is based on demos and a few sparse data points (like Klarna), so the next 12 months will be important in having businesses show real results from AI improving efficiency.

Will AI help incumbents in services just as much?

There’s one important counter argument to this: won’t everyone, incumbents included, benefit from AI? If incumbent services businesses use AI to improve their R&D efficiency and cut their operations costs, will AI really help startups grow large and compete? AI’s impact so far has clearly been to favor incumbents like Google and Microsoft.

I think there’s some truth to this argument. United Healthcare is probably going to get more efficient from AI in both their R&D velocity and operations. But on a relative basis, I think AI is going to help startups much more than incumbents in tech-enabled services.

NFX has a great framework on thinking about where AI will advantage startups vs incumbents.8 AI is likely to help incumbents in industries which:

Move fast

Are tech savvy

Have processes only marginally improved by AI

Don’t have a business model conflict from AI

Incumbents in services industries, like health insurers, clearly don’t fit this category. They move slowly, are not tech savvy, and can have their processes significantly improved by AI. They also have a bit of a business model conflict given the natural messiness in letting go significant Opex headcount from their existing employee base.

This is why it’s such an exciting opportunity for these startups, but also for tech’s ability to solve important real world problems. All the same problems that tech founders identified 10 years ago in real estate, insurance, healthcare, and similar industries are still there: poor customer experiences, high prices, and little innovation. If AI can bring new promise to these industries, it will not just be great for investors in these companies but it will be an important win for the tech sector as a whole.

I’m defining these businesses more broadly than traditional professional services (like law, accounting, etc.). I’m including businesses in insurance, real estate, hospitality, etc. Basically anywhere where you aren’t selling software or goods and your business is labor intensive.

Fintech has some successes with neobanks (Nubank, Sofi) and brokerages (Robinhood). And there are some promising startups, but VC returns from this category of startups have clearly been poor.

There are plenty of other challenges, but this is one of the biggest.

Regulations can make services businesses very profitable if they can build software and processes that satisfy them - look at United Healthcare or JP Morgan’s market cap. But they also famously make it difficult for new entrants, like startups, to enter the market.

Simple model, obviously there are lots of other factors to consider here.

I expect customer support inquiries to go way up with AI too, but on net we should still see a decline in customer service employment

I think there are open questions about how durable this margin improvement will be and whether it will just be competed away between startups. Software businesses have high margin not just because they have zero marginal cost but also due to switching costs, network effects, etc. Topic for a future post!

Similar framework is sustaining vs disruptive innovation