Why Waymo won't crush Uber anytime soon

Variable demand for ridesharing will make it hard to challenge Uber

Conventional wisdom is that Uber is screwed because of autonomous vehicles. Can they really compete with Waymo or Tesla when human drivers are the biggest cost for ridesharing trips?

I used to have this view until I read through Uber's Q4 earnings report released last month. In it, they (pretty convincingly) argue they have an underrated advantage: the highly variable nature of ridesharing demand makes an AV-only network challenging to operate profitably.

If true, that means Uber is likely to remain the best marketplace to get a ride (whether human or AV) for a long time.

Uber’s Edge: Variable Demand

Uber argues that AV commercialization will take a long time because five different parts all need to go right. The first four are 1) super-human safety, 2) clear regulations across states and countries, 3) cost-effective hardware, and 4) efficient on-the-ground operations.1

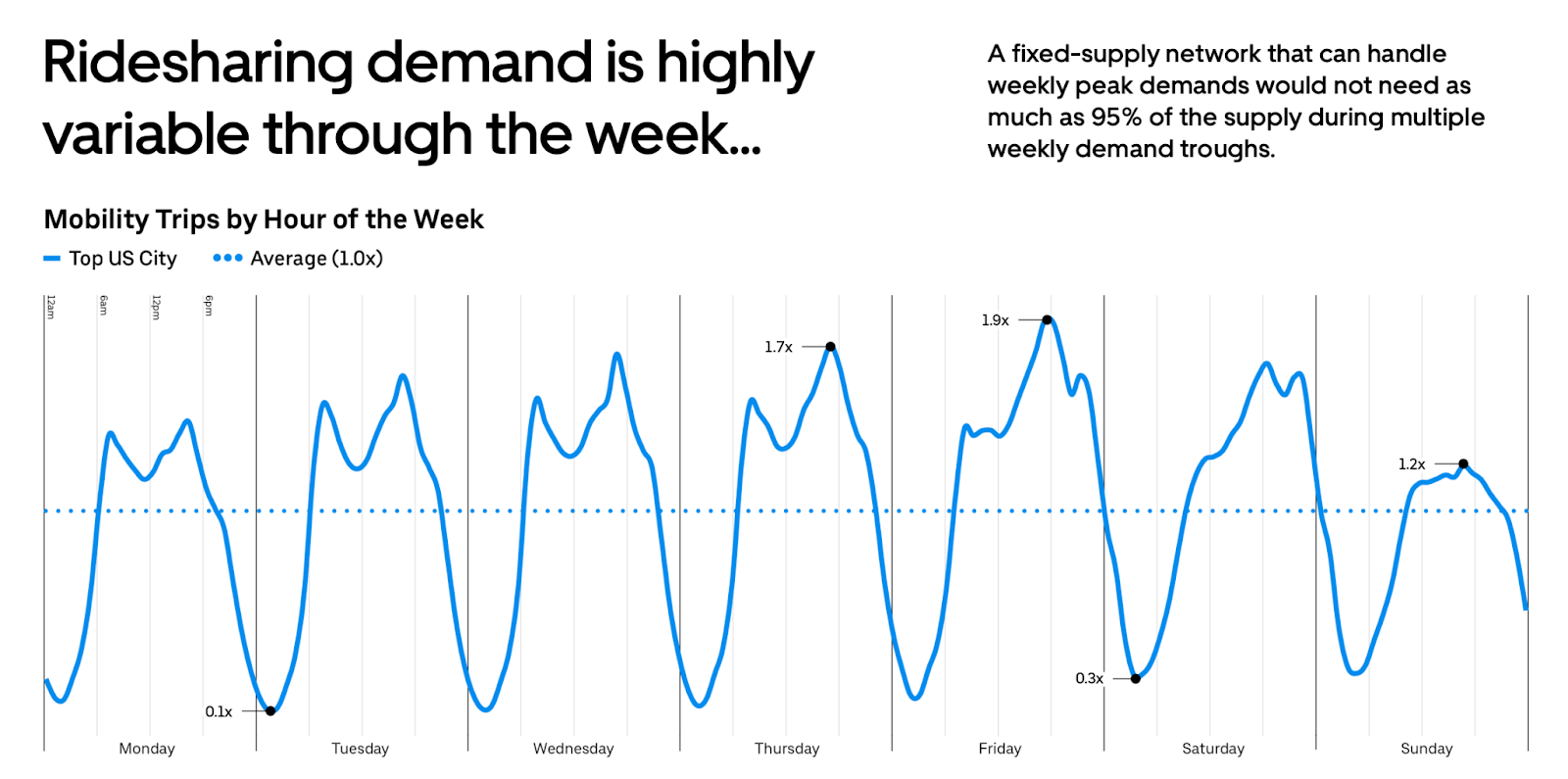

But even if AV companies get all four of these down (which is doable over the next 5 years), there is a more daunting fifth challenge: variable ridesharing demand. From Uber’s Q4 earnings:

Finally, assuming that all four of the aforementioned commercialization issues have been addressed, AV operators will face another daunting challenge: the highly variable nature of ridesharing demand, which has large peaks and troughs throughout the day, week, month, and year. Any standalone player with a fixed depreciating asset will need to build against that reality: choosing between running a highly underutilized network (if supply is built for peak demand) or a highly unreliable network2 at peak periods (if supply is built for anything less than peak).

For Uber, this isn’t a problem because they don’t have to manage a fleet! Uber drivers naturally come and go from the platform to meet demand spikes and there isn’t the same cost to Uber from a driver’s car sitting “idle” when they are not working.3

This is why Uber expects the optimal ridesharing network to be a mix of human drivers and AVs, even in the long run. As Uber CEO Dara Khosrowshahi told Ben Thompson of Stratechery:

We think the best way to do that, and certainly in the early days, is a hybrid of this base layer of autonomous supply, so to speak. That is then, on top of that, you’ve got humans who come in and out during peaks. The great thing about humans is, while they will eventually be more expensive on a cost-per-mile basis than let’s say a machine, you only pay for their utilization when they’re actually working, whereas with an AV, you pay, it’s kind of fixed4

An Uber-run marketplace of human + AV drivers is already being tested out in a few of Waymo’s markets. In Atlanta (and recently launched Austin), Waymo is available exclusively in Uber’s app and Uber is also handling things like vehicle cleaning, repair, and other general depot operations.

Waymo’s Path to Lower Costs

This is a pretty daunting challenge for Waymo, the main Uber competitor for AV, but they could overcome it if they bring costs down enough. To give an extreme example, if Waymo’s cost per mile were 1% of Uber’s when highly utilized, it wouldn’t really matter if their cars sat around underutilized because Waymo would be so much cheaper than Uber and their stand-alone network would win.

How cheap would they need to be to compete with Uber?5 Uber today is at roughly ~$2.00 per mile in the US, per their Q4 earnings. If Waymo was half that cost per mile (~$1.00), even meaningfully lower utilization could make Waymo still better priced than Uber.

Today, they are far from that. There’s no great data, but various estimates put Waymo’s costs today at somewhere between $2.00 and $3.50 per mile (so likely higher than Uber).6 A good chunk of this is operating costs, like maintenance, servicing, cleaning, insurance, charging, fleet management, etc.7

But the bigger challenge is reducing car depreciation costs. Bank of America estimates current vehicles cost ~$140k and have a useful life of 200k miles, which puts depreciation costs per mile (excluding maintenance, service, etc.) at ~$0.70 alone. Other estimates go as high as $1.00 per mile. The higher the car cost, the higher the operating costs as well (think more costly repairs, insurance, etc.)

So Waymo has no chance of building a successful standalone marketplace without a much cheaper car. They know this, which is why they partnered with a Chinese automaker Zeekr for their 6th generation car (coming soon) which is likely to be much cheaper. China’s Baidu announced a ~$30,000 USD autonomous vehicle late last year, so it seems plausible that Waymo can get its costs down significantly too but it won’t be easy.

What about Tesla?

If high hardware costs and managing fleets are the problem, what about Tesla? Their cars are much cheaper, they can produce them at scale, and they can leverage their customers' existing cars to rent them out on their robotaxi platform without managing a fleet. Problem solved?

This could be its own piece, but I’ll keep it short here: leveraging customer vehicles gives Tesla an advantage and I think they are better positioned than Waymo. But I expect customer opt-in to be low for a few reasons:

Earnings are likely to be low after accounting for repairs, depreciation, electricity, etc.

Tesla owners (like all car owners) value the certainty of having their cars available at all times. Imagine renting out your car and it gets in an accident and now you don't have a car. Or it gets stuck in traffic and now it’s not available to pick you up.

It’s the same reason most car owners don’t rent out on Turo.

Ridesharing demand peaks at the same time as personal car usage, which means their pool of cars to tap into is shrinking just as they need them.

This means Tesla is most likely going to have to rely on fleets just like Waymo for most of their trips (they are using fleets exclusively for their Austin launch). Still, Tesla’s ability to tap customer vehicles to handle peak demand on top of fleets will help (similar to Uber tapping humans), so Tesla has a better shot at building their own marketplace. But it’s still a question of where the math shakes out.

Uber’s beneficial position

Highly variable demand in ridesharing creates a big challenge for AV-only networks that won't go away anytime soon. This means AV companies have two options:

Partner with Uber and accept being one supply source in a broader mixed human/AV marketplace. I expect OEMs outside of Tesla to go this route.

Achieve such dramatic cost reductions (to $0.50-$1.00/mile) that the utilization penalty doesn't matter and they successfully build their own marketplaces.

Most will take Option 1 (prediction: Zoox), not just because it’s hard to build your own marketplace but the math will be hard to pass up. As Dara notes in the same Stratechery interview:

We take 20%, we pay the driver 80%. If you just look at it mathematically, that means that if we drive a utilization benefit of 25%, we’re paying for ourselves.

Option 2 takes a lot of capital, though if anyone can pull it off it’s Waymo (with Google's backing) and Tesla (with its manufacturing scale and fundraising ability). Waymo’s progress in SF so far shouldn’t be discounted.

But the bull case for Uber in 2025 is stronger than I expected. Just like people pay the Google and Meta “tax” today to reach their customers, we may see AV companies paying the “Uber tax” going forward to reach theirs.

Appendix:

I attempted to measure Waymo’s existing utilization from the data they are required to report in California. The methodology is a little complicated (see here for more) but I estimate Waymo’s utilization in California to be around 30% last summer, the last time we had data reported.

That compares to around 55% utilization for Uber in NYC (where data is readily available). So far, Waymo seems to running at lower utilization, but we’ll need to track this data more closely as they ramp up operations.

Uber argues that they are uniquely positioned to work with their AV partners to solve these challenges, but I’m less convinced. Waymo has already shown its stellar record on safety (1) and the regulatory frameworks will eventually get sorted out (2). Hardware costs are also likely to come down dramatically (3) and I think fleet management is a skill Waymo or others can learn (4).

Waymo could decide they will just have much higher ETAs at peak demand (and lower prices) than Uber. But the additional challenge here is that riders have shown they are relatively unwilling to trade off time for prices in ridesharing historically. That is, they probably prefer $20 and 5 min eta over $15 and 20 min eta. This makes the variable demand problem even harder and means Waymo doesn’t have a lot of room to work with.

The big advantage Uber has is that its drivers have lower depreciation costs than someone would if they were buying cars and using them 100% for ridesharing. In that case, ridesharing earnings have to fully justify the cost of the vehicle.

But Uber drivers usually need a car anyway so the earnings they get just need to be worth the additional miles traveled on the platform and not justify the entire cost of the car.

There are analogies to the power market that Uber likes to make here.

My basic assumption is that people are not willing to pay a material premium for Waymo over Uber, but that remains to be seen. There is also a separate question of how cheap Waymo would need to be to compete with personal car ownership, which I may address in another piece.

All the examples I found: Uber says >=”>2.00,” Altimeter estimate pegs it at $2.60, Bank of America is at: $1.30 (no link), JMP: 3.50 (?), a Reddit guesstimate puts it at $2.00

I went down a bit of a rabbit hole with car rental companies here because similar to AV companies they need to 1) manage a fleet of vehicles 2) clean, repair, and maintain them 3) deal with swings in utilization.

I couldn’t find that much useful in terms of data. Avis says its operating costs (excluding depreciation) are ~$36 per day per vehicle (revenue is ~73 per day and operating costs are roughly half that) in the US. But there are no miles data and it’s hard to get any more granular data.

That said, the fact that these companies seem to have gotten costs down pretty low is a good sign for AV companies. Fleet management for AV companies is more challenging/expensive in many ways (more costly hardware, higher turnover than rentals), but you also amortize these costs over more miles, you don’t have to pay for staff to reposition cars, and you don’t need to pay for costly parking/real estate in premium locations.

Great analysis!

Long-term, I think that self-driving taxi operators could largely capture times of peak demand because the depreciation can just be spread out out over the 10-year life of the car rather than only going for full utilization and hitting 300k miles after just 2 years.

But I agree that the the extra capital cost of self-driving taxis is a key limiting factor right now. For this reason I think adoption might only be about one third as fast as the initial adoption of rideshare in the 2010s.

I built a chart you might appreciate here: https://www.2120insights.com/i/152869747/medium-term-is-the-price-right

Thank you. This is a very useful post. Short and sweet. Makes me bullish UBER. I have no position though. I mean I can buy both GOOG and UBER. :)

I got a question: How about Waymo going all in once costs are down enough? They can develop their own marketplace (most people have Gmail / Google Play accounts + add google maps, etc). They can decide to license google maps for commercial purposes and earn royalty, etc. This helps offset some of the costs. I compare this with YouTube (it took a long time). A standalone YouTube company was less likely to pull this feat. What do you think?

Reference 2: "Waymo could decide they will just have much higher ETAs at peak demand (and lower prices) than Uber. But the additional challenge here is that riders have shown they are relatively unwilling to trade off time for prices in ridesharing historically. That is, they probably prefer $20 and 5 min eta over $15 and 20 min eta. This makes the variable demand problem even harder and means Waymo doesn’t have a lot of room to work with."